While most of us were running around like headless chickens in February trying desperately to wrap up our tax affairs, after a year that saw more carnage than arguably any other year that we’ve experienced to date, hardly any of us noticed that the markets chose largely to ignore our personal, financial, political and pandemic woes of the past 12 months and to forge on to new (and in some cases, all time) highs.

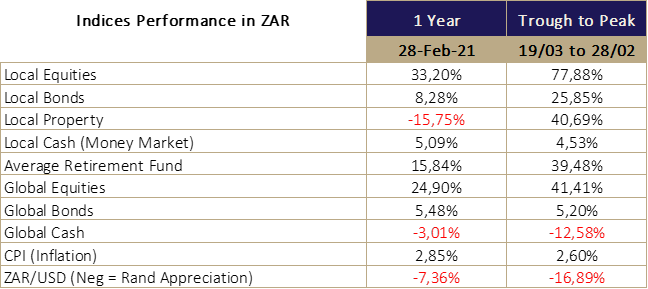

It has proved, once again, how important it is to stay the course and invest through the cycles. A jumpy investor who disinvested at the bottom of the market would have missed a market bounce-back (from trough to peak) of 77,8% on the JSE.

The local market is now 10% up from previous highs in January 2018 (interesting fact: 2 years prior to Covid).

While the lead-up story in offshore markets, differs remarkably, the end result has been similar with the MSCI World index up 41,4% over the same period, up 15% from previous highs in February 2020.

After six years of relative underperformance, retirement funds are back to their longer-term average returns.

Perhaps most surprising to South Africans, was the rebound of the rand from over R19 to the dollar to a low of R14,38 the other day. Amazing how quickly emotion can take over and how quickly South Africans conclude that “we’ll never see R16 to the dollar ever again”.

If only we had brought money back at R19 to the dollar and then invested in the JSE. You’d have nearly doubled your money, yet no one dreamed of doing that.

The principles of investing will persist through the cycles. While it’s natural to be discouraged by our current political landscape, it’s important to try to drown out the noise and stick to sound investing principles.

Additionally, you can control the aspects of your plan that are controllable, such as your monthly investment amount and adjust your plan periodically (i.e. increase your investment) for the aspects that are out of your control (i.e. the markets returned 6% instead of 10% as per my plan). None of the above gets us any closer to deciding where (now) to put our hard-earned money going forwards. What it should allude to though is that the long-term strategy you and your adviser decided

on last year, the year before or five years ago (if not opportunistic at the time) should prevail through the cycles. Albeit that sometimes those cycles may have to be extended due to unforeseen circumstances. Therefore:

- Don’t put 1 year money into a 10-year strategy (or bitcoin).

- Don’t pull 10-year money out after only 3 years.

Goal-focused and outcomes-based planning should be at the core of what you do with your hard-earned cash and an appropriate level of assets class exposure is essential to achieving the outcome.

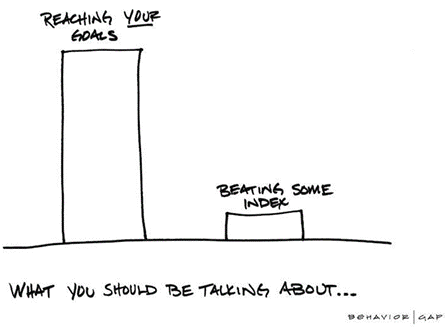

Have you heard the saying: “Only 6% of South Africans will retire comfortably”? Well, that number has sat at 6% since as far back as I can remember (and long before that). With so much emphasis recently being placed on the investment eroding nature of high product fees and the new age, low-fee products entering the market, surely this figure should have improved by now? Why hasn’t it?

The answer is actually quite simple. It has less to do with fees or returns, and more to do with the fact that only 6% of South Africans understand the principles of investing and that meeting your goals are more important than the return or the fees of the investment (both of which are largely out of your control).

Meeting your goals is less dependent on the aspects that are out of your control (like beating an index) and more dependent on the aspects that are in your control (like disciplined investing and sticking to a long-term strategy).

As Carl Richards, author of The Behaviour Gap, says; it is possible to beat every index, every year and still not meet any of your financial goals, while at the same time it is possible to have the worst luck from an investment perspective and still meet your financial goals because of careful planning and a disciplined investment mindset. At the end of the term, which of the above scenarios are you going to be happier with?

If the investment goal was a comfortable retirement, then Mr Index-Beater can only watch from his work desk (where he still sits with his bad back) while Mr Disciplined-Investor drives past to the airport with his kids and grandkids in tow for their annual holiday in Mauritius.

In our last newsletter we asked the question; ‘Is now a time to be looking to capitalise on the strong rand and move some funds offshore to diversify?”

I haven’t gone as far as to answer this here, as every investors situation is different. We believe a diversified approach, depending on your own personal situation, is important and so a careful analysis of your circumstances is important before deciding to move funds into an offshore strategy.

However, we continue to receive queries about offshore opportunities and in this regard, we have found some very promising-looking offshore investment options. At the same time, with the rand looking to remain reasonably stable, we hope this provides us the time to help you to implement some diversification in your portfolios should you be interested in this option.

We look forward to interacting with you on your path to securing true intergenerational wealth for you and your family.

Please don’t hesitate to contact either Hugh or Bruce from the Investing Department to discuss your path forward.