WHY EMPLOYEE BENEFITS?

If the covid-19 pandemic has taught us anything, it is the importance that our health and wellness plays in meeting our goals. And as businesses this translates to the health and wellness of our employees too.

People are the crucial system that underpins your organisation’s ability to grow and thrive and so the question here is; “How crucial are employee benefits to helping to achieve these goals?”.

The answer: They are extremely important!

Some research shows that up to 80% of employees would rather have new or additional benefits instead of a pay increase. Benefits aren’t just desirable to employees. They can improve your business. The benefit to the employer is undeniable. Not only are you able to provide an employee and their family with cash or other forms of compensation at a time of desperate sadness or need, but offering benefits can increase loyalty, focus and productivity, attendance, health and morale and can reduce your employee turnover thus saving more in recruiting costs.

Who should have employee benefits?

While insurance benefits are usually associated with higher income earners; simple and easy to understand “core” benefits can provide great value to lower income employees too. For example, simple funeral cover for an employee and his family can create unmentionable peace of mind for that employee and can be done at a fraction of the cost to the business as opposed to in the employee’s personal capacity. South Africa has a relatively advanced funeral cover industry largely due to the cultural importance placed on the burying of a loved one. While the individual products are more comprehensive than most employer offered cover, costs can be in excess of R110 to R150 for the primary member only as compared to R10 to R40 to cover the employee’s entire family on an employer scheme. At these prices, an employer can add considerable value to employees and their families, and most should be willing to do so since often the first point of call for financial assistance for a bereaved family is the employer of their breadwinner.

So, what are the most important benefits to provide your employees?

When referring to Employee Benefits, we are talking about benefits such as;

- Retirement Funds,

- Life Cover,

- Disability Cover,

- Critical Illness or Trauma cover,

- Income Protection (for disability and illness),

- Funeral Cover,

- Health care benefit (Medical Aid and other medical insurance).

There are various factors that need to be considered when determining which benefits to provide for your staff such as employee demographics, affordability (both by the employee and employer), job descriptions and the size and type of your business.

Different employees would also find certain benefits more desirable than others. For example, a 45 year old married breadwinner with 3 children will need a lot more life cover than a 21 year-old graduate who is still living at home and has no dependants. Both of them however have an equal need for income protection to provide them with and income should they be unable to work for a short period (or even permanently) due to an illness or injury (whether obtained at work or not). So, an important decision for the business to make is what the minimum amount of cover to be offered will be. This should be made in consultation with a professional and perhaps even with the employees themselves through a poll or questionnaire to find out what benefits would be most valued by them.

The standard employee benefit template of:

- An Employer Retirement Fund PLUS

- Life Cover, usually of 3 times the member’s annual salary

- Income Protection of 75% of monthly salary, and

- Funeral Cover (various amounts) for the staff member, his or her spouse and their children,

while certainly not suitable for all types of employees, is in fact a reasonable starting point.

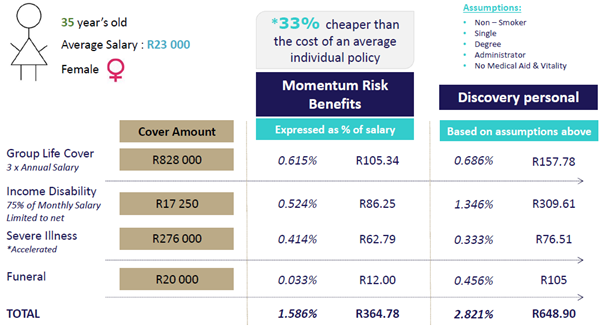

This level of cover could cost, depending on demographic again, anywhere between 1% and 5% of payroll and is generally substantially cheaper than an individual insurance policy thus adds value to all staff up to director level (see example below).

Employer Retirement Fund versus Retirement Annuity.

For your higher income staff, an Employer fund usually offers a more cost effective and tax efficient option to save for retirement.

For your lower LSM staff, it has the additional benefit of offering a cash withdrawal option should they resign or be dismissed (retirement annuities are only accessible after age 55). This appeals to a large demographic in South Africa who need this windfall to make ends meet during periods in between employment.

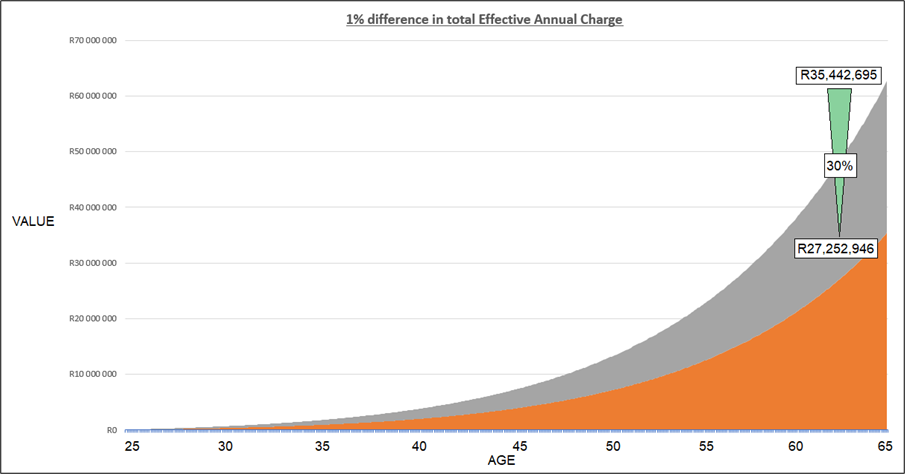

By far the greatest advantage though is the costing within the fund and the significant difference these costs can make to the member’s total capital, an therefore income, at retirement.

Regardless of the criteria or your businesses specific needs, there should be a certain level of benefits that will appeal to your staff and implementation thereof can go a long way toward showing your commitment to them and hence growing their loyalty to the business and its management.

The beauty of the product is that you can tailor your offering to suit your staff or different categories of employees to offer the best value and peace of mind to your most valued asset, your human resources.

Should you like to explore some options, please do not hesitate to contact our investment division.